Purchasing Property under a Trust

Purchasing properties within Trusts comes with a number of benefits. This is also generally the way people are able to buy 10 or more properties due to the positive effects Trusts can have on affordability, if set up correctly.

Please consider watching the video - it contains all the information but is a little easier for me to explain when I can talk/write and show you in real time.

Benefits of buying Properties within a Trust

We'll break down each of the benefits in-depth further down the page.

| Advantages or purchasing within a Trust: |

|---|

| It can be very beneficial for affordability. This can result in practically limitless affordability if done correctly. |

| Generally tax efficient for distributing profits. |

| Lower land tax on large portfolios (can be higher on 1 - 2 properties). |

| Asset protection. |

| Overall - usually cheaper on large portfolios. Depsite the setup and ongoing fees associated, the tax benefits generally outweigh the costs in the long run. |

| Disadvantages or purchasing within a Trust: |

|---|

| Setup costs: about $2,000 per Trust |

| Complexity: a much higher learning curve |

| Ongoing Accountancy fees: around $2,000 p.a. |

| Higher land tax for 1 - 2 properties in most States. |

| Negative gearing effects are trapped in the Trust - this can be a benefit, but is generally better to avoid. |

Increasing Home Loan affordability using a Trust (or Trusts)

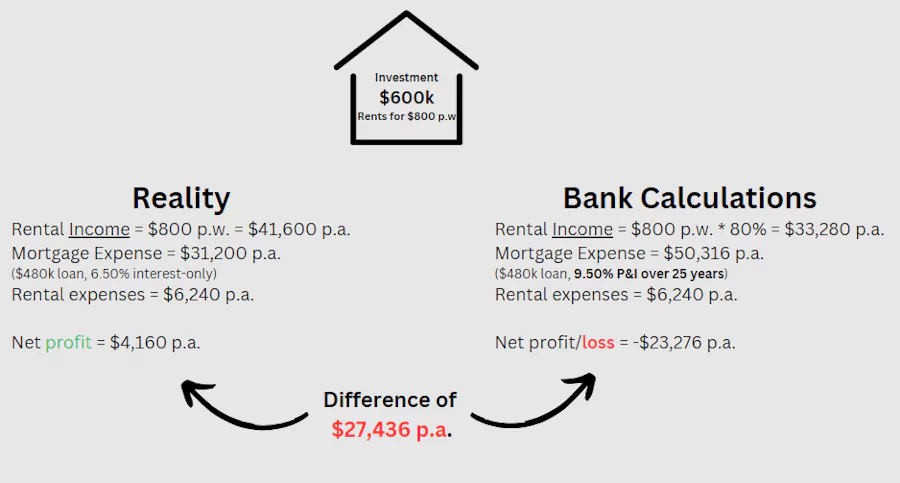

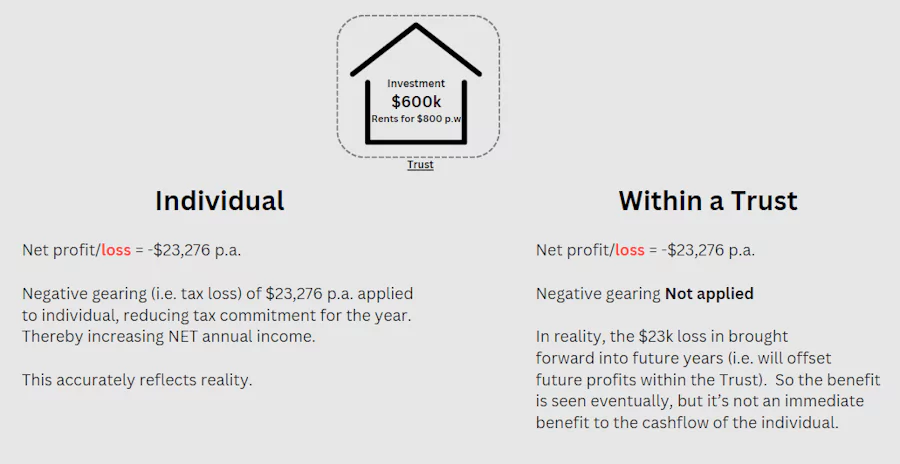

Let's first understand how a bank assesses your income/expenses relating to an investment property, when owned as an individual

The above example shows a positively geared property, and yet it is still considered a $23k p.a. liability by the bank's calculations. This is because, as a general rule, the lenders will:

- Buffer the interest rate by 3% (i.e. actual rate of 6.50% + 3% = 9.50%)

- Only take 70% - 90% of the rental income

- Ignore the interest-only repayments, and instead amortize the loan repayments over the P&I term. For example, a 30 year term w/ 5 years interest-only would instead be considered as a 25 year P&I loan

- Still take rental expenses on top. As a minimum, they'll usually take 10% - 20% of the income as expenses (that's on top of only taking 80% of rental income)

The effect of these calculations becomes extremely detrimental for most investors after just 1 or 2 properties.

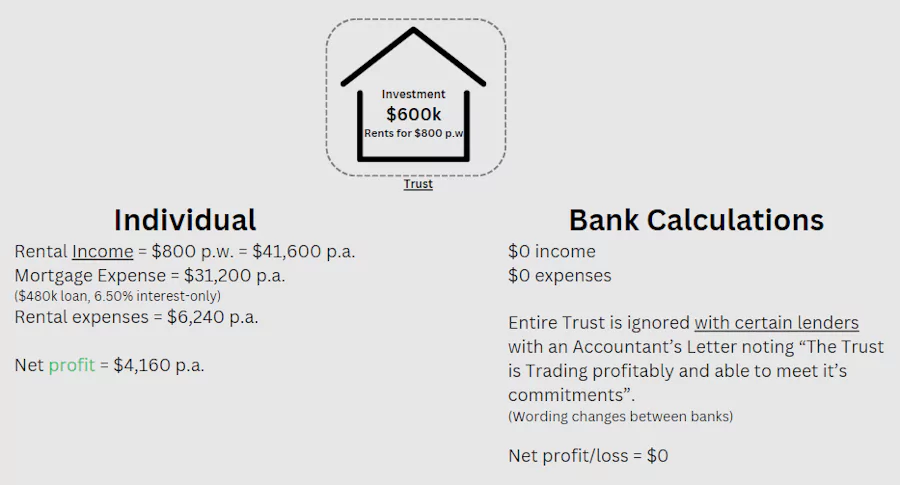

Using a Trust, some lenders will actually let us ignore the income & expenses of that Property - or in actuality, ignore all income/expenses of the Trust in full. Most people believe it's better to include a positively geared property in the application, but that's seldom the case.

Let's look at how we could increase cashflow by $23k per year (according to the banks' calculations) if we instead had that property within a Trust:

In the above example, we've gotten rid of the $23k assumed loss by instead providing an Accountant's Letter stating "ABC Trust is trading profitably & able to meet it's commitments". Most Accountant's are happy to sign this off for a positively geared property, and certain lenders can then ignore the Trust in full, which removes that alleged $23k loss p.a. This means that the property within that Trust has no effect on your affordability.

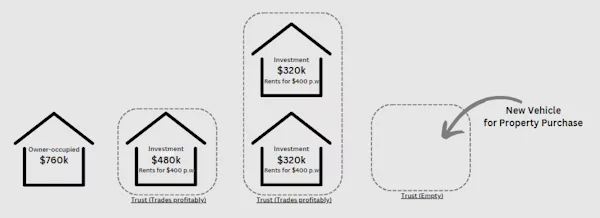

How do people buy multiple investment properties?

We can use the above knowledge to start seeing where people fail or succeed in purchasing 10+ properties. Unless very positively geared, each property in an individual name will have a negative effect on affordability. This effect generally means that even relatively high earners get capped out at 2 or 3 investments.

Lets have a look at the below 'investment tree'. Each level (as you go down) is where you add 1 property to the portfolio.

Lets breakdown the different paths people can take:

- Maxing out affordability on PPOR (left branch): if you do this, you need to wait for income/expenses/rates to become more favourable before you can purchase an investment, whether in your name or a Trust. Unfortunately this is a necessary first step for a lot of people that don't want to 'rentvest'.

- Maxing out in your individual name with PPOR and/or investment property(ies) (2nd branch): this is not a necessary step, and is a trap/mistake for most people (don't worry, everyone does it). You're now stuck - you can't purchase any more properties in your own name or in a Trust. We'll talk about how to fix this later. This is often the best option for people just looking to purchase 1 or 2 investment properties over their lifetime.

- PPOR in own name, 1 investment in own name, then the rest in Trusts (3rd branch): this is a really good option if affordability allows. Keeping 1 property in your name can be beneficial for Land Tax reasons (explained further down), and you've left suffificent affordability to purchase in Trusts indefinitely. There is a benefit to having extra affordability left in the bank, which we'll look at later.

- PPOR in own name, all investments within Trusts (4th branch): probably the best scenario for most people looking to build a portfolio. This gives you a lot of flexibility regarding borrowing power. Your affordability has not changed (if that property is positively geared), so you can rinse-and-repeat another 10 times, if you'd like to.

This shows how affordability decreases every time you purchase an investment property in your own name, until you get to $0 (unless the properties are very positively geared), and also shows how affordability is unaffected by properties within Trusts (if positively geared by $1).

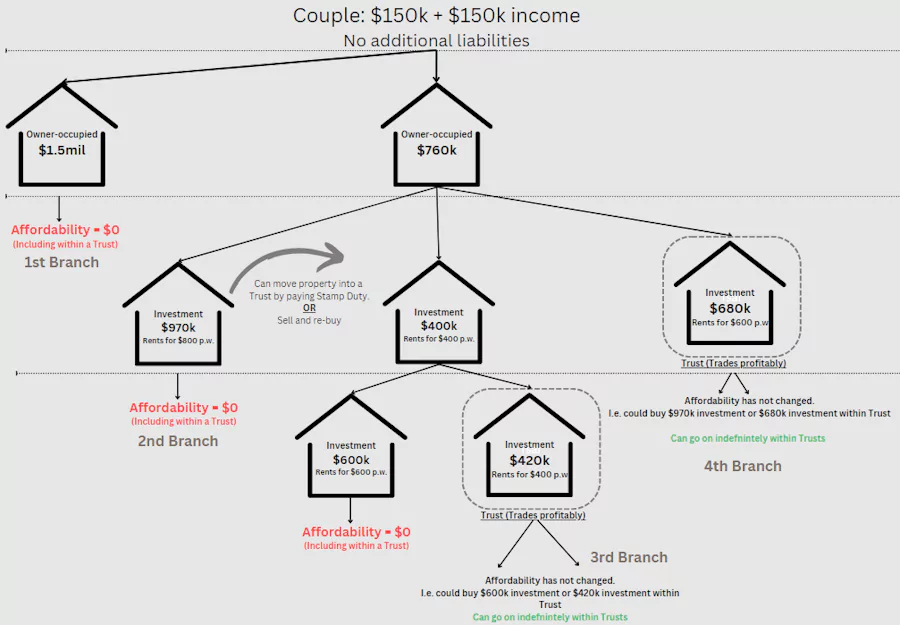

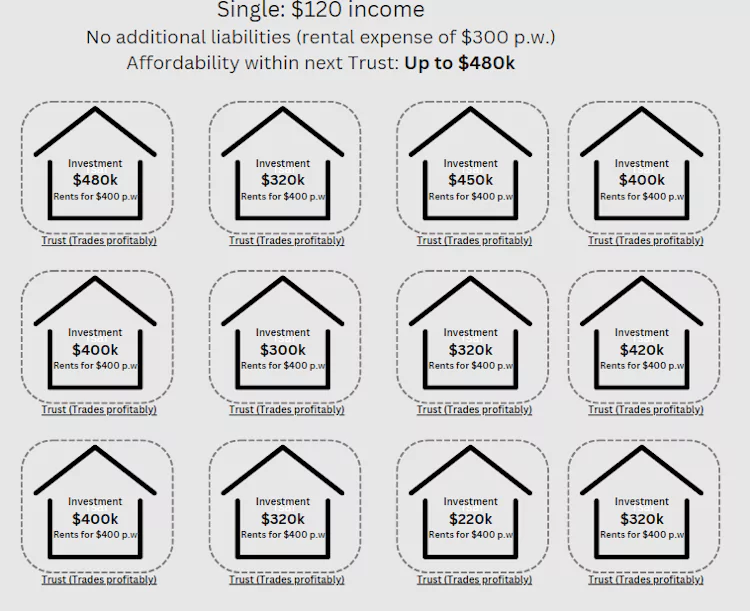

How do people buy 10 investment properties?

The below is an example of how a single person on $120k income can own 12 properties and still have affordability to keep going. As long as each Trust is trading at a profit, their affordability is unchanged. Again - only a select few banks will allow this - so don't assume you can go anywhere and not declare these as liabilities. Your Accountant also has to be comfortable signing a letter for each Trust.

What if you've already maxed affordability?

If you've maxed your affordability because you already own investments in your personal name, unfortunately there are only a couple of options:

- Sell an investment property. This frees up affordability & capital, and you can then start purchasing all future properties within Trusts. Selling costs & Stamp Duty are a major cost here - but it's still generally my preferred way to fix this - as it ends up with a cleaner end situation. If you have a PPOR mortgage, we can use debt recycling to restructure your debt and ensure 100% of the investment purchase costs are tax deductible, and as little as possible is non-tax deductible debt.

- Move a property into a Trust. If you think you have a great property, you can refinance it into a Trust instead of selling. This is a full loan application which unfortunately also triggers Stamp Duty.

- Do nothing. You can sit on your property if you have no plans to purchase more in the future, or you can wait until you've paid it down and/or rates/rents have changed in your favour. This is a slow strategy to build a portfolio, but works for some people.

Why is affordability lower in a Trust?

To preface this: the affordability across your whole portfolio can benefit greatly by using Trusts, however your personal maximum affordability is always higher than (or equal to) what you can buy in a Trust. You could, for example, buy a $970k property in your own name, or a $680k property in a Trust. The Trust is still beneficial as you can potentially borrow $680k in each of 100 Trusts.

So why is affordability lower in the Trust?

In the above, the 'bank calculation' shows a $23k loss per year (even though it's realistically positively geared). When calculating your personal affordability, that $23k is considered a tax deduction, so your net income reduces by less than $23k ($15k, for exmple). When calculating affordability within a Trust, the negative gearing is not applied, so the full $23k is applied to the affordability calculations.

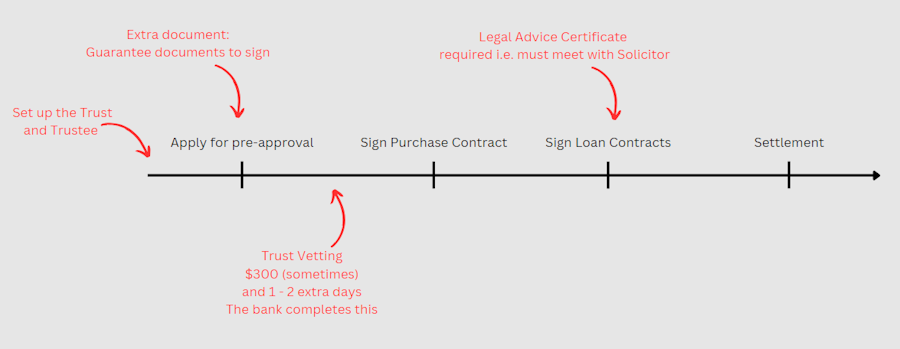

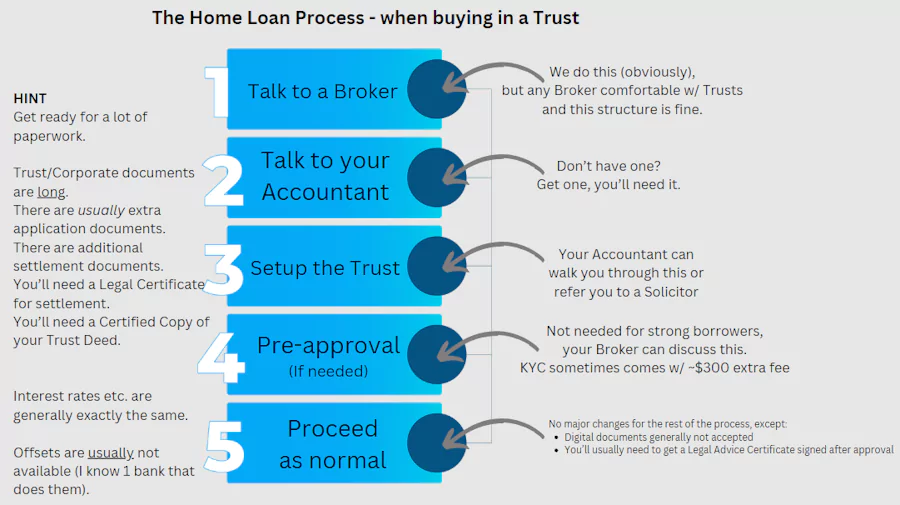

The Home Loan Process in a Trust

The process for a home loan within a Trust is not too different to a normal home loan. Generally - there are more documents required (Certified Trust Deed) and more documents to sign - but nothing too major - and your Mortgage Broker should be able to walk you through it. But it's important to note that we can't get a pre-approval until you have the Trust set up, but we can (and should) still check eligibility before you spend any money getting the Trust and Trustee prepared.

The bits highlighted in red are the additional/different steps when getting a home loan in a Trust name.

Who is the Borrower / Guarantor for a Trust mortgage?

The borrower for the home loan depends on the set up. Generally, a Corporate Trustee makes more sense for lending purposes - but your Accountant may advise otherwise.

- Corporate Trustee: The Corporate Trustee is the borrower in their own right and as Trustee for the Trust. The Individual(s) are Servicing Guarantor's (you and/or spouse, generally) i.e. we will use the individual's income to show that we have sufficient income to afford the loan.

- Individual Trustee: The Individual is the borrower in their own right and as Trustee for the Trust.

Who is the Purchaser when buying in a Trust?

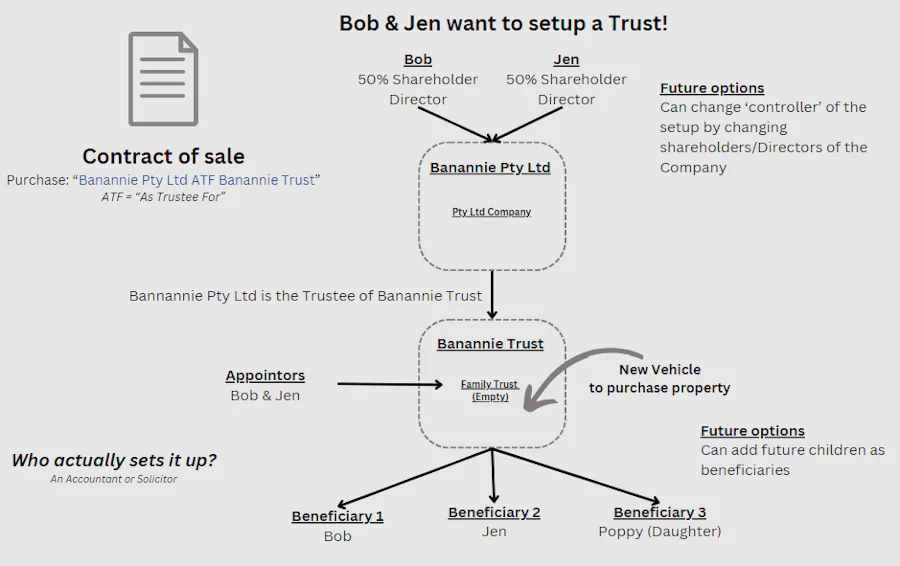

This sounds obvious i.e. the purchaser should be the Trust, but that's not quite right. The Trust can't own property in it's own right, so the Trustee owns the propery on behalf of the Trust "As Trustee For". Here's what should actually be on the Contract of Sale when buying the House:

- Corporate Trustee: Purchaser would be "My-New-Company Pty Ltd ATF My-Family-Trust Trust"

- Individual Trustee: Purchase would be "John Smith ATF My-Family-Trust Trust"

- Optional alternative (talk to your Solicitor) if you don't yet have the Trust set up: Purchaser on the Contract can be "John Smith or Nominee". You can then later complete a Nomination Form to 'nominate' "My-New-Company Pty Ltd ATF My-Family-Trust Trust" as the purchaser.

Documents needed for a home loan in a Trust

On top of the usual documents required for a home loan, you'll also need:

- Certified Trust Deed. Request this when you set up the Trust and keep it safe - it's a nightmare if you lose the original.

- Certificate of Duty (in some States) - this is evidence that you paid the Duty when setting up the Trust.

- Some banks will charge additional fees for a Trust. This is usually a $300 (roughly) "Trust Vetting Fee".

What are the risks of buying multiple properties within Trusts?

The risks of buying 1 or 2 properties within Trusts are no different than if you did it in your own name. The risks come with the ability to purchase more properties than you usually would. It can become a trap if you no longer have affordability to refinance or equity to sell down. When a Trust stops being profitable, it can no longer be excluded from future home loan applications (including refinances). This means that it may mean you're unable to refinance anything, and everything will swap over to P&I - which may cause a domino effect i.e. more Trusts become unprofitable, thereby making it more difficult to refinance (or impossible). A few risks to consider:

- More exposure to Real Estate: this can mean greater financial gain, but also greater financial loss

- A number of Trusts running at a loss can result in significant losses

- Greater risk from interest rate rises

- Future changes to bank's Assessment criteria may make refinances impossible

How to reduce risk significantly:

- Keep equity available. The bigger the portfolio/exposure, the more equity you may opt to keep in each property. This gives you the option to sell down any unprofitable Trusts, should you need to.

- Always assume your interest-only loans will change to P&I. Whilst we may be able to refinance back to interest-only, we may not.

- Always assume interest rates will be going up. Ensure you're comfortable with a 3% interest rate rise.

What happens to the negative gearing within the Trust?

Lets say you lose $20,000 in the first year, net $0 in year 2, profit of $10k in year 3, and profit of $15k in year 4. Here's what that might look like. I say 'might' because I'm not an Accountant - so this should be checked directly with your Accountant before making any decisions.

- Year 1: Loss of $20,000 in Trust Tax Return (TTR). $20k needs to come from the individual's post-tax funds to cover expenses and is listed as a beneficiary loan (i.e. the Trust owes the individual $20k). $20k loss is carried forward to future tax years.

- Year 2: $0 profit/loss. $20k loss carries forward in TTR. No input/output to/from the individual.

- Year 3: $10k profit. $10k returned to individual as a loan repayment which is a tax-free amount (i.e. individual doesn't pay income tax on this as they put in post-tax funds originally). $10k loss carries forward.

- Year 4: $15k profit. As we have a $10k loss brought forward, $10k is repaid to the individual as a tax-free loan repayments, and $5k is distributed to the individual as taxable income (i.e. goes on to the individual's tax return as taxable income). $0 loss to bring forward.

In the above example, the benefit of negative gearing is seen, however it's somewhat delayed to future years. This can be beneficial if you're on a higher tax bracket in future years, however I generally consider this a disadvantage of purchasing in a Trust as it would be better to improve immediate cashflow for investment purposes.

Once the Trust is turning a profit, the tax benefits of a Trust can start making a huge difference to cashflow.

Distributing profits from a Property Trust

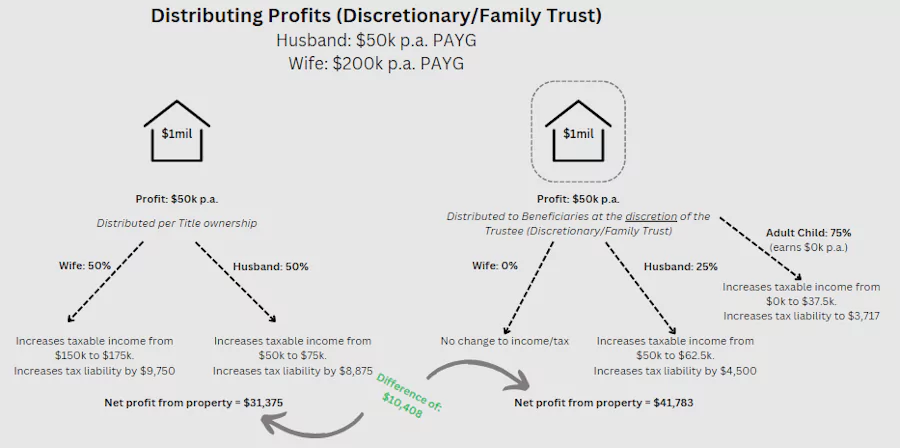

A Discretionary Trust (a Family Trust is a type of Discretionary Trust - to avoid confusion) has discretion over how it distributes the profit each year. Depending on the income structure of your household, this can have huge tax implications.

Without the Trust, the profit is always distributed per the Property Title. Now you can do an uneven split of the Title to try and make the distributions more favourable (generally you want 25%+ per borrower), however you can't change this easily at a later date. The Discretionary (or Family) Trust can distribute the profit at it's discretion each financial year and change how it distributes each year. It can also distribute to other beneficiaries: most commonly these are the children, but can be anyone depending on the Trust setup. In the above example, we can reduce the tax liability by $10k per year by using the Trusts discretion of distribution. This effect is minor (or non-existent) where there's only one beneficiary or all beneficiaries are on a similar income.

Using a Trust to distribute pre-tax dollars to assist children

The ATO is clear that the funds distributed to the child must be for the child's benefit. For example, you can't simply distribute to the child, then ask them to give you the dollars back. Nevertheless, the above example is a great way to try and help your children later in life. Instead of giving them your post-tax dollars as a gift, you can instead distribute pre-tax dollars to them at 18 or over (possibly whilst they're studying and earning $0).

What about Unit Trusts?

Unit Trusts are a bit different and don't have the same benefits. Instead of Beneficiaries, a Unit Trust will have Unit Holders. This is more commonly used for non-related parties that want to invest together (it is a great option, if this is something you want to do). A Unit Trust has no discretion in distributing profits, but has all the other benefits from a lending point of view.

If two friends, Miranda & Penny, purchase a property together in a Unit Trust, they'll likely own 50 Unit each (essentially 50% each), which means they'll each be distributed 50% of the Profits each year.

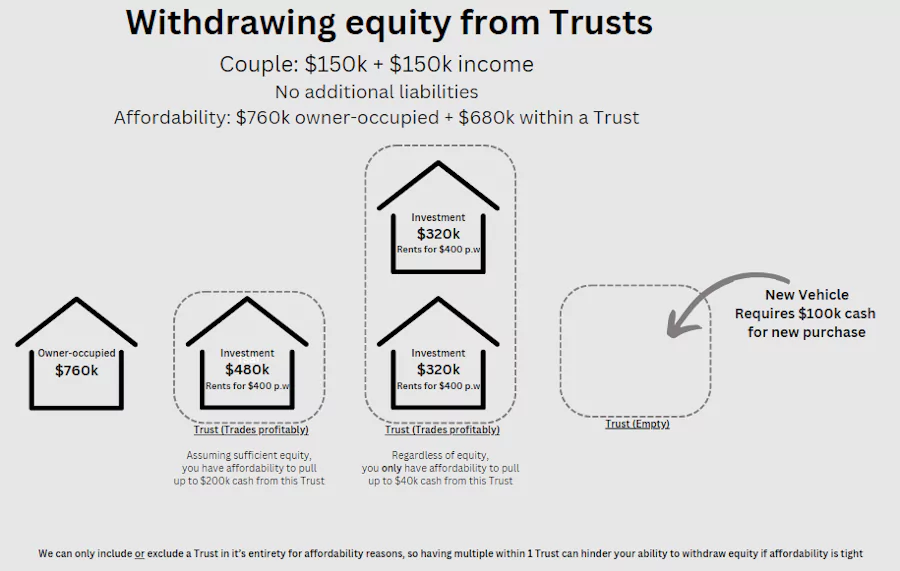

Withdrawing Equity from Properties in Trust

An important concept here is that when applying for a home loan, we can either:

- Include the Trust in full i.e. all income and expenses (which will be shaded/buffered as normal). OR,

- Exclude the Trust in full.

We cannot pick-and-choose which properties/mortgages within a Trust we want to include/exclude - it's all or nothing.

Depending on how comfortable your affordability is, this can mean it's best to have only 1 property in each Trust.

In the above example, the individual(s) have only got affordability for $680k within any Trust. As they've put 2 properties in their 2nd Trust, they can only withdraw $40k equity no matter how much equity is 'available', as they already have $640k in home loans within that Trust. They can withdraw up to $200k cash from their first Trust (if the equity is available), as they're well below their borrowing limit.

The lesson here: we want to keep an affordability buffer in each Trust to ensure we can draw out equity if/when we need it.

In an ideal world, we actually have an affordability buffer of 1+ properties. This allows us to withdraw equity from 1 Trust (thereby 'exposing' it to the bank's affordability calculations) and get a pre-approval/formal approval for a purchase property at the same time. If we don't have a sufficient affordability buffer, we instead need to get the equity out (excluding the future purchase-Trust), then ask for a new Accountant's Letter and apply for a pre-approval / formal approval (excluding the Trust we just got the cash from). It gets pretty complicated - but the short of it is that everyone's life is easier if you have a large affordability buffer i.e. don't max yourself out anywhere.

The cost of using a Trust to buy property in Australia

| General additional costs for using a Trust to purchase property: |

|---|

| Approximately $2,000 to set up the Trust. |

| Approximately $2,000 in additional Accountancy fees per annum. |

| Sometimes, there is an additional fee for getting a home loan within a Trust. This is generally around $300 for Trust Vetting. |

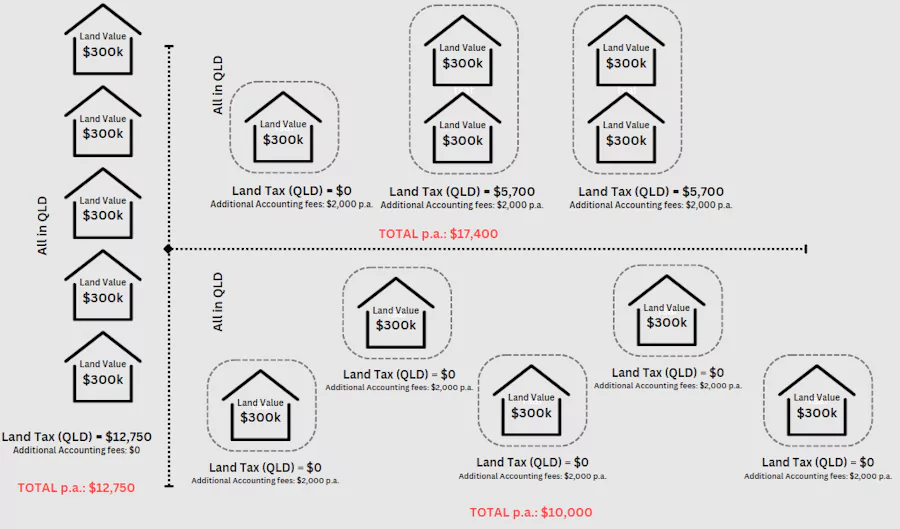

Land Tax when purchasing property within Trusts

This varies State-to-State. Again, I'm not an Accountant so have a chat to them before making decisions - but this is definitely something to consider and plan for.

As a general rule: Land Tax is calculated on the value of the land and is calculated individually for each entity. Individuals often get a higher Tax-free threshold and/or lower Land Tax Rates. The more property within any one entity, the more the land tax goes up (exponentially, sort of).

The above shows three alternate setups for owning 5 properties within QLD. You'll see the Trusts pay very high Land Tax once they go above the threshold in QLD, and the individual (left column) pays very high land tax for owning so many in one entity. Even with $2,000 per Trust in Accountancy fees, it works out cheaper having each property in its own Trust.

How many properties per Trust?

You can save a small amount in Accounting fees by putting in more than 1 property into 1 Trust, where appropriate. This would require careful planning with your Mortgage Broker and Accountant. If in doubt, consider doing 1 property per Trust initially. You can always add extra properties to those Trusts later, if it becomes more suitable to do so.

How to set up the Trust for a Property Purchase

To set the Trust up, you need to talk to an Accountant/Solicitor. Sometimes your Accountant will do it in-house, other times they'll refer you to an external Solicitor. You need to make sure you set up the correct type of Trust and general structure. You can use the below as a guide:

| Generally accepted Trust setup for a mortgage: |

|---|

| Discretionary or Unit Trust |

| Trustee: Individual(s) or Corporate Trustee |

| For Corporate Trustees: Individual(s) to be Guarantors |

| For Individual(s) Trustees: Individual to be the borrower in their own capacity and as Trustee for the Trust |

| The Trust should be a non-trading entity: meaning it's setup specifically for investment (not a trading business) |

| Own less than 5 properties |

| Have only Natural Persons as the beneficiaries |

| My preferred Trust setup for a mortgage: |

|---|

| Discretionary Trust |

| Corporate Trustee |

| Individual(s) to be Guarantors |

| Trust / Company setup exclusively for Property investment |

Example Trust setup for Property

There's a few important roles to consider:

- Trustee: The Trustee owns the property on behalf of the Trust "As trustee for" and makes operational decisions about the Trust. This can be a person/people, or a Company. A Company adds an additional layer between the asset and the individual, as an individual Trustee would own the asset As Trustee For the Trust.

- Assuming a Corporate Trustee: the Shareholders have ultimate Control of the Company, where the Directors manage day-to-day operations. These are generally the same person/people for Property investing.

- Appointors of the Trust: These have ultimate control of the Trust as they have the ability to appoint a new Trustee.

- Beneficiaries: these generally want to be natural people for property investing (i.e. no Bucket Companies), and are the individuals that will benefit from any profits. This generally will include yourselves, but may also include other family members.

Getting a Home Loan in a Trust

The actual process for getting a home loan under a Trust is not that different to the normal home loan process. The tricky part is usually the planning of what/how to achieve your goals - a Financial Planner may help with this.

The initial steps require planning. If you know you're a strong borrower with strong borrowing power, you don't necessarily need to talk to a Broker upfront. If you're unsure - they can give you estimates for affordability inside/outside a Trust so you can make better decisions. Then, you need to talk to an Accountant about the correct Trust structure to suit your situation, the fees involved, and the tax implications (now and in the future). Once you know what you want to do, you need to setup the Trust and Trustee (if a Corporate Trustee). This must be done before you can apply for a pre-approval. You can technically do this after signing a contract (and a few people do), but setting up a Trust can take 1 - 2 weeks which eats into the Finance Clause timeline.

From there, the process is much the same. Just note:

- Digital documents are generally not accepted

- Prior to settlement, you'll usually need Legal Advice

- Note: the Contract of Sale would need to say something to the effect of "New Company Pty Ltd ATF My Family Trust"

- There is extra paperwork in the home loan process

- The Trust/Company documents can be very long and cumbersome - just keep that in mind as it can get overwhelming

How to get started purchasing Property within Trusts?

Honestly, just give me a call or send me an email. We can generally have a chat upfront, but then I'll need to know your aims/goals before I can start helping you formulate a plan. Someone that wants to buy 1 property every 5 years is very different to someone trying to buy a property every 6 months. And someone with a large buffer on affordability will generally have a lot more flexibility in how we set things up. Whilst we don't charge for our services (paid by the bank), we do ask for your information/documents upfront, which generally takes 20 minutes. We'll then spend a couple of hours doing a full review and then we can have a productive chat about what you can or can't do.

You don't need to be close to us geographically, we can assist anyone in Australia.

DISCLAIMER: You must not rely on the information in the report as an alternative to financial advice from an appropriately qualified professional. If you have any specific questions about any financial matter you should consult an appropriately qualified professional. We do not represent, warrant, undertake or guarantee that the use of guidance in the report will lead to any particular outcome or result. The content, calculations and opinions contained in this article are of the writer only, and are not necessarily those of Blue Fox Finance.

Zak AveryOwnerMortgage Broker

About the Author

Zak has been a Mortgage Broker since 2015, and founded Blue Fox Finance in February 2017. He has all industry memberships, qualifications, insurances and has received over 100 5-star Google reviews.